by Sonia Oprean

I took the first steps towards a financial career ten years ago when I joined one of the world’s largest financial services firms. At the time, even though I had studied them at university, I failed to see the practical application of concepts such as business diagnosis, financial and management accounting.

My interests gravitated towards more appealing and less technical fields, such as management and marketing. I knew, however, that in order to understand how the economic engine of any business works, a sound understanding of the financial sector would be critical.

Over the following years I persevered in the area of financial analysis, largely thanks to a colleague who became my friend and mentor, and who made sure I was focusing on gaining a strategic understanding of finance and accounting concepts. She opened my eyes to the dynamics of stock management and showed me how to translate highly technical financial terms in simple language that even non-experts could understand.

My career in financial services involved working on over 40 audit projects, often in charge of coordinating teams in clients’ offices. I worked on audits of companies worth hundreds of millions of euros, I dealt with both growing companies and insolvent businesses across a variety of sectors, from the automotive industry to consumer goods, freight transport, healthcare and many more.

First contact with social enterprises

When I made the transition to working with social enterprises, I was convinced it would not be difficult to make a success of this new financial model and my own career move. After all, I had dealt with notable and major corporations. How difficult could it be to work with much smaller albeit different type of business?

In reality, I spent many of those initial months trying to understand the most pressing and complex challenges within that sector. This new hybrid-financing business model that aimed for social impact was fascinating to me. Though different than traditional business, a social enterprise is still first and foremost a business, and in order for it to be successful, it needs to ramp up its economic drivers.

In the past six years, I have met many ambitious, hands-on, highly-focused entrepreneurs who use all the available knowledge resources and work tirelessly on their company performance and understanding its financial factors. I’ve also encountered others who were ultimately defeated by the constant struggle to understand the more technical sides of the business; some frustrated by their dealings with their own accountants, others humiliated by their own investors on account of failing to deliver convincing multi-annual financial projections.

In this article I will attempt to touch on the most important aspects of financial analysis for social enterprises seeking financing. My aim is to help increase the confidence of entrepreneurs and social enterprise managers in understanding financial modelling so that they can have an informed conversation with their partners, such as impact investors [1].

Financial modelling for social enterprises is a James Bond-like mission … if James Bond worked with spreadsheets. There is no easy way to tackle this as the conversation always revolves around the “real” costs and how high they are. To most questions, the answer will most often be, ‘It’s more complicated than that …’.

Actual operating costs of NGO-type social enterprises

The first social enterprises in Romania were founded by experienced NGOs aiming to increase their financial sustainability and reduce their dependence on donations. This trend continues today, 10-15 years later, when many successful social enterprises are operating within established NGOs.

Such NGOs have many revenue streams, some linked to their non-profit activities, i.e. donations, grants and subsidies, others from selling goods and services. Most often, these NGOs invest their revenues into their social programmes, such as providing employment to vulnerable people. It often takes a long time for these social enterprises to become profitable, during which time the parent NGO finances their operating costs via external grants and subsidies. Other times, profitability is not possible, especially for social integration-type enterprises whose costs must be at least partially subsidized in order to provide job creation for vulnerable people.

When impact investors assess the profit/loss accounts of an economically active NGO, they will find that the economic activity is profitable and generates surplus cash for the parent organisation, without realising, at first glance, that the organisation itself is in fact likely to cover part of the operating costs of the social enterprise through an external grant. In other words, part of the operating costs of the social enterprise may be unintentionally “hidden”.

In this case, the financial assessment of the economic activity might not accurately reflect the performance of the social enterprise. This is due to a number of reasons, namely: the complexity of the financing contracts framework, particularly when it comes to framing projected operating costs; the lack of in-depth financial management knowledge within the parent organisation, and not having separate management systems for the economic and non-profit activities, respectively.

Other types of subsidised costs are those covered by the social enterprise arm within an NGO through the use of volunteer resources: for example, the production manager works pro bono (temporarily) for the social enterprise, or the office of the social enterprise is provided free of charge by a supporter of the parent organisation. Irrespective of their duration, these costs must be taken into account when determining the actual operating costs of the social enterprise itself.

Building a financial model for social enterprises is a difficult task. The usual tools used to measure profitability for traditional businesses, such as the trial balance, do not necessarily help. It is almost impossible to determine the real operating costs of a social enterprise without corroborating additional qualitative and quantitative information, such as funding contracts, production reports, guidelines and regulations, organisational structure and, last but not least, extensive interviews with the social entrepreneurs themselves.

Three ways to assess the real costs of running a social enterprise

All social enterprises have a social mission, and therefore face a number of additional social costs, which I detailed here. Firstly, and most importantly, any social entrepreneur needs to know the nature and level of social costs, and understand their impact on profitability.

When seeking funds for expansion, social entrepreneurs will often negotiate with third parties, such as investors or bank representatives, on the basis of financial statements. Given the realities described above, this interaction may lead to confusion and mistrust on both sides, and may ultimately end up fruitless.

Nevertheless, there are a number of minimal best practices that social enterprises can use to gauge and measure the real operating costs and help potential investors perform an accurate assessment of the business.

- Establish separate and adequate management for the non-profit and the economic activity in order to generate a clear picture of the actual cost structure and the overall operating costs for the entire organisation.

- Maintain an operational record of production for the economic activity detailing sales volumes, variable costs and price per unit, production costs. This information will give an accurate overview of the financial cost per unit and overall, will help determine profitability per product.

- Perform periodical reconciliation between operational and financial statements. This will showcase the organisation’s financial and operational control and will help increase the confidence of potential investors, who like to see maturity and stability over time in a business.

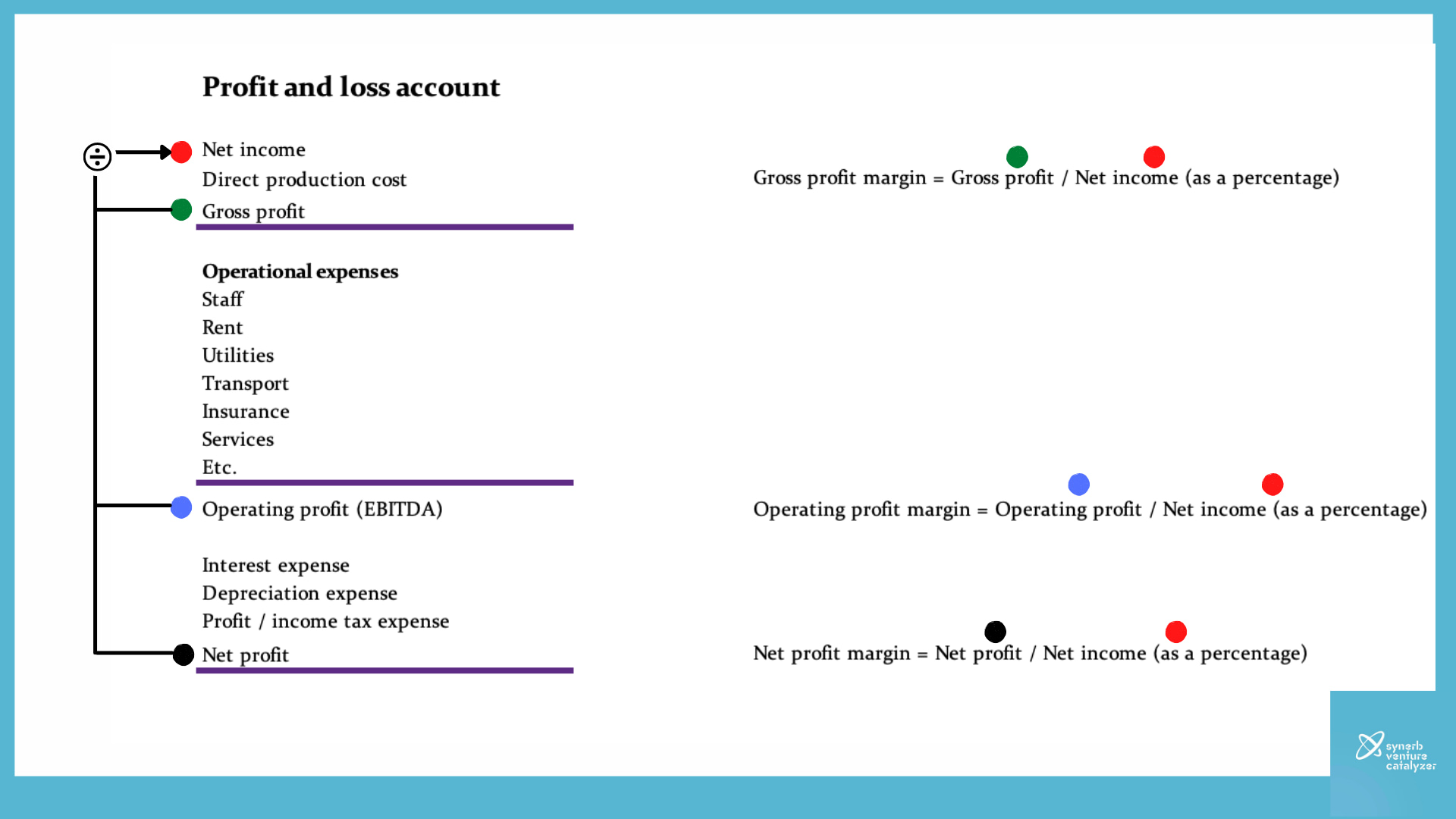

Three key profitability indicators: gross profit, operating profit and net profit

Any social enterprise not using the three best practices recommended above, could have major difficulties in measuring its profitability. Note that profit indicators may also be skewed if the financial data does not accurately reflect the financial situation of the social enterprise.

Only by using data collected and corroborated across separate administration and operational records of production, coupled with the practice of financial reconciliation, can give the social enterprise the necessary tools to develop a simple financial model, as shown in the figure below.

Gross profit [2], i.e. the difference between net income (excluding VAT) and costs directly attributed to production, is the first indicator of operational sustainability.

The gross profit margin indicates what percentage of net income represents gross profit. It can vary by industry and location, i.e. there is no “standard” gross profit margin, but it must cover operational costs.

Example: for business models with large staff (bakeries, restaurants), an acceptable gross profit margin would be at least 50%, as the highest percentage of operational expenditure is staff costs.

Operating profit, known as EBITDA [3], is the surplus available to cover financial expenses and depreciation, after covering operational costs (staff, utilities, transport, insurance, etc.). The operating profit margin is what percentage of the net income represents operating profit.

Net profit means pure profit, after all expenses related to the enterprise’s activity have been deducted, including depreciation, interest and taxes. The net profit margin shows what percentage of net income represents net profit.

EBITDA and social enterprise profit margins

Having gone through a financial assessment process for a loan or investment funding, many social entrepreneurs may be more familiar with EBITDA than net profit. They may also have pondered why operating profit is so important for investors.

Operating profit is a better financial indicator of operational efficiency than net profit, as the latter is affected by expenditure outside of management’s control or results from financial decisions taken before the evaluation period.

Example: investing in state-of-the-art technology for a healthcare entity will most likely generate, depending on the amortisation period, high depreciation charges in the years following the investment. At the same time, if the same company has taken loans in a foreign currency or has a variable interest rate loan, it will incur higher or lower financial costs depending on national or global macroeconomic dynamics outside of its control, but which affect the exchange rate or interest rate. Net profit is also subject to tax rate variations.

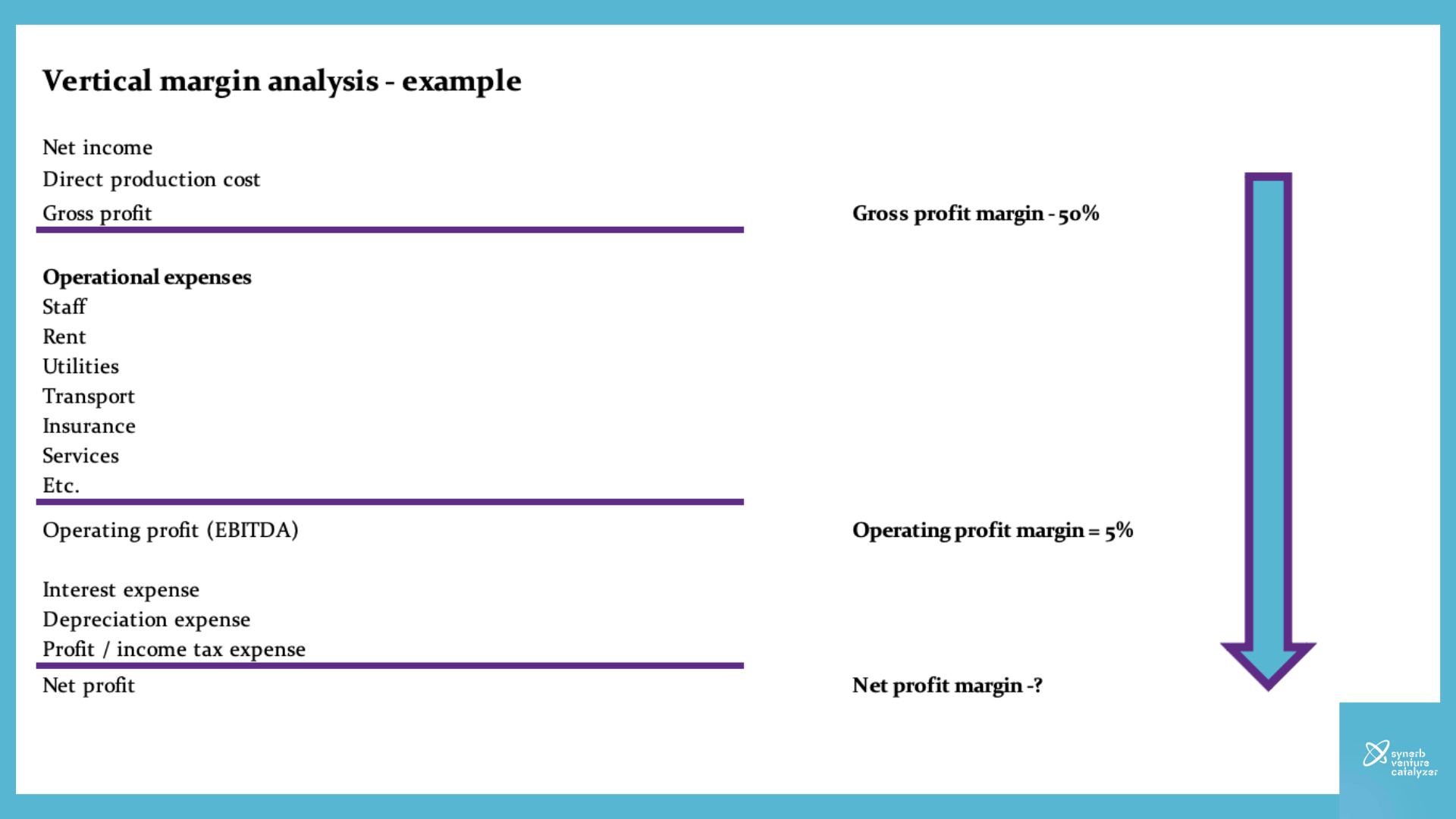

A vertical analysis of the gross, operating and net profit margin is the best way for social entrepreneurs to understand which costs erode its profitability. A low gross profit margin generated by high production costs may raise questions about the financial sustainability of the initial design of the product/service, the efficiency of the production process or may impose growing to scale as the only strategy possible to achieve profitability.

Gross profit margin calculation directly affects an enterprise’s business model and many social entrepreneurs are keen to rethink it on that basis. A significant difference in profitability margins (for example, 45% – resulting from 50% gross profit margin and 5% operating profit margin) certainly requires an in-depth assessment of what operational costs tend to dry up resources.

Last but not least, a social entrepreneur needs to pay attention to the social costs of the business.

Example: An environmental social enterprise has higher than average production costs as it most likely uses more expensive, sustainable sources, which in turn results in additional social costs. If this enterprise charges average-level market prices, it will have a lower gross profit margin. Therefore, its financial performance is lower when compared to a similar but for-profit enterprise that does not have an environmental social mission.

Number crunching and impact investors

Regular funding opportunities or needs will arise over the lifecycle of a social enterprise. Many times, social entrepreneurs or managers of social enterprises approach me with this question, ‘A funding opportunity has just opened up that fits well with our activity and objectives, but we usually generate low profit, and sometimes a loss. Would we be eligible?’. To which I almost always respond, much like a potential investor would, ‘What are the reasons behind this low financial performance, and how will the funding help you fix that?’.

On the one hand, if social entrepreneurs are able to explain the low gross profitability of their business, they can also explain the nature and need of its social costs to any potential investor. On the other hand, an impact investor will want to know that his financing solves a social problem and will help the organisation grow. Nevertheless, where growth is not realistic, the investment could be earmarked for business consolidation, which is when impact investors assign short-to-medium term funding to resolve financial difficulties before growing the social enterprise overall.

Before sitting down with any potential investors, social enterprise owners and management need to have a clear understanding of the underlying causes of the financial difficulties, how these are reflected in the business’s financial model and have a realistic plan to overcome these.

*

[1] The impact investor strategy will take into account financial revenue as well as the social and environmental benefits of the business.

[2] Many financial and impact investment resources are in English, so in this article I will use certain key terms in English. This is to help social entrepreneurs become familiar with international terminology.

[3] Earnings Before Interest, Tax, Depreciation and Amortisation – Profit before interest, taxes and depreciation.