by Sonia Oprean

The social entrepreneurs who contact us to discuss their financial performance often have the same profile: they are running an established social enterprise – usually three or four years old – and are in a rut in terms of their financial performance.

These entrepreneurs set up their social enterprise with the aim of generating a surplus to support a social cause. Their perception, shortly after reaching break-even or even before that point, is that their enterprise has reached a plateau beyond which it can no longer grow.

Large cost cuts are not possible because the organization deliberately incorporates the social costs in the business model. Growing sales is often problematic. Over time, social entrepreneurs test two to three market niches, change two to three sales managers, but find it difficult to grow their customer base past the few thousand loyal customers mark. These loyal clients repeatedly buy products from them, mostly because they are committed to the social cause of the enterprise.

As a general profile, many social businesses operate in the field of consumer products, where competition is fierce, preferences change rapidly and profit margins are small. When supporting these enterprises, we use a financial performance assessment framework that generates a new perspective on the social business, and can lead to making relevant strategic decisions that over time will increase the financial sustainability of the enterprise.

What is a business driver?

The daily operations of any social business is influenced by many factors. Some of these factors are the key factors that can drive important changes in the business performance. They are called “key business drivers”, internal or external factors that have a major influence on the operational and financial results of a social business.

Most entrepreneurs are aware of the drivers that are specific to their businesses. For example, in case of a restaurant, the maximum seating capacity is a key business driver that can determine the size of the revenues. A similar business driver for a social enterprise that provides home healthcare is the number of skilled employees or collaborators providing home healthcare services. For a small craft workshop selling home decoration items through an intermediary – such as an online aggregator – a key business driver will be the variety of products offered and the commission charged by the intermediary platform.

Monitoring key business drivers

A key business driver is rarely static and it is exerting variable degrees of pressure on the business, often determining the financial performance in unexpected ways. The influence and impact of some factors is not immediately evident nor necessarily visible in the day-to-day operations of the businesses. An analysis of the key business drivers can provide important clues about existing market dynamics, customer preferences, supplier behaviour, and over time revealing new trends. All these can provide valuable input for better financial projections.

The importance of analysing the balance sheet variations and financial profitability indicators

An entrepreneur who has been through a negotiation process with a bank or with an investor, after providing the financial statements of the last few years, most likely has been confronted with many questions about the variations in the different balance sheet categories.

.Questions such as “Why has the revenue from services decreased between year 2 and year 3?”, “Why have production costs increased in the last year?” or “Why have personnel costs progressively decreased in the last 3 years?” might have some simple and straightforward answers that are within the entrepreneur’s reach. But the discussion with funders rarely stops at this point.

Balance sheet variations and the analysis of the financial profitability indicators gives a true picture of the company’s past financial performance. This historical data, along with the dynamics of internal or external factors, can help us anticipate the response of the business model to different pressures – in effect, it helps us create different financial scenarios. Hence the importance of this analysis.

Let’s take the example of a social enterprise that sells accessories or fashion items. The fashion industry is an industry that “consumes” creativity. A business operating in this sector will need to design new, creative clothes or accessories, aligned with the trends of the year. Another feature of the industry is that, a few months after the collection launch, fashion items will most likely be sold at discount. The interest of any social business in this industry is to sell as many products as possible at the full price, soon after launching a collection.

Let’s take the example of a social enterprise that sells accessories or fashion items. The fashion industry is an industry that “consumes” creativity. A business operating in this sector will need to design new, creative clothes or accessories, aligned with the trends of the year. Another feature of the industry is that, a few months after the collection launch, fashion items will most likely be sold at discount. The interest of any social business in this industry is to sell as many products as possible at the full price, soon after launching a collection.

In the profit and loss account of a business of this type, discount expenditure is a highly important cost category to track, for two reasons: 1) To ensure the profitability of a product range, it is important that the products, even during the discount sales period, are not priced below the direct cost of production; and 2) If the percentage of the discount expenditure in the yearly income increases each year, it means that the business is under pressure to offer larger discounts in order to sell its products. This might be a sign that the business is becoming less competitive on the market. Moreover, if the post-season revenues tend to exceed the revenues earned shortly after launching a collection, customers have most likely formed a habit of buying the fashion items at a discounted price. It becomes obvious that the company will have to reassess its position in the market and come up with a strategy to avoid the imminent erosion of profitability.

In the profit and loss account of a business of this type, discount expenditure is a highly important cost category to track, for two reasons: 1) To ensure the profitability of a product range, it is important that the products, even during the discount sales period, are not priced below the direct cost of production; and 2) If the percentage of the discount expenditure in the yearly income increases each year, it means that the business is under pressure to offer larger discounts in order to sell its products. This might be a sign that the business is becoming less competitive on the market. Moreover, if the post-season revenues tend to exceed the revenues earned shortly after launching a collection, customers have most likely formed a habit of buying the fashion items at a discounted price. It becomes obvious that the company will have to reassess its position in the market and come up with a strategy to avoid the imminent erosion of profitability.

Which variations do we need to track to understand the evolution of a social business? How to monitor the dynamics of key business drivers?

Income and expense structure. Before carrying out a variance analysis, it is critical to understand where the revenue is coming from and how it is being used. “What are the most important revenue streams and what is their share in the total revenue amount? What are the expenses directly related to the generation of those revenues? And what is their share in total expenses or in relation to the revenue stream (gross profit margin per product)?” These are questions that every entrepreneur should be able to answer easily after a short analysis of the financial statements of a social business.

If you want to read more about some important financial indicators, read the article I have written, here.

Annual changes in income and expense. As a simple rule of thumb, once we identify and understand the most important revenue and expense categories from our financial model, we should track their year-to-year variation, in absolute and percentage changes.

Let’s take an example of a social enterprise that sells educational materials for children with special needs (accounting for 60% of total revenue) and which also provides educational services for children with special needs (40% of the total revenue). By analysing the evolution of these two revenue streams, the social enterprise finds that the revenue from the sale of educational materials increased with 5% per year. The income from educational services has remained constant in absolute terms.

This 5% increase in sales generates some hypotheses:

1) The customers are kindergartens and schools. They have become more inclusive and enrol more children with special needs in their classrooms, hence the need for more adapted learning materials.

or

Any of these hypotheses might turn out to be true. The variation itself shows us that an existing niche market is growing or that there is a new category of interested customers. Clearly, as a result of this analysis, our strategy should include researching the market niche in question and focusing our sales efforts to capitalize on these growth opportunities.

The direct costs variations should be consistent and proportional with the revenue variations. A disproportionate increase of the direct costs with a rate much higher than the revenue growth might suggest, for example, higher prices of raw material, losses due to sub-optimal technological processes, or the use of new recipes based on more expensive raw materials.

Every scenario I highlighted above is a decision point for the company. An increase in the prices of raw material will confront the company with the decision to either pass on this cost to the final consumer, by increasing the final selling price, thus risking losing customers, or to keep prices unchanged and lose part of the profit margin. Increased direct costs due to technological losses require rapid intervention to restructure some processes or improve the training programmes for the production team. These actions must be taken to avoid the continued decrease of the margins.

When the blue ocean turns red

Many of the social enterprises I have worked with started out in a niche market, selling products with a high value-add or services in a market with few players, relying on a loyal customer base and the prospect of growing this niche clientele. This favourable market scenario is known in the economic literature as the ‘blue ocean’.[1]

Important: declining trends in revenue and profit margins should be carefully monitored from year-to-year within a social enterprise, even when these variations seem only minor variations. On the long run these minor variations may indicate that the market is starting to become crowded, and the social enterprise is heading towards an imminent “red ocean” scenario.

What can, in such a scenario, a social enterprise do? Given the limited funding opportunities available to social enterprises in the current Romanian ecosystem, it is highly unlikely it will secure the capital to make significant investments in the enterprise and strengthen its position in the market. Most often, facing market “threats” and using its limited resources wisely remains the only way to go.

New avenues

An in-depth year-to-year financial analysis of the evolution of key income and expenditure categories and key financial indicators will help the social enterprise to correctly forecast trends, anticipate imminent threats and prepare in advance its strategy to face market challenges.

Product portfolio analysis

We have seen a number of business models that showed limited growth potential. What would be an adequate course of action for the management of a social enterprise that produces at the level of 80-90% of its capacity, sells everything produced, has already optimised costs – without a drift from the social mission! – but aims nevertheless to increase its profitability by at least a few percent?

In these situations, we usually work with the social entrepreneurs to conduct a product portfolio analysis. We assess how much each product or service contributes to the overall financial sustainability of the organization in relation to the position of each product or service in their customers’ preferences, looking at the historical sales levels.

Important: when a business operates close to full capacity, managers have very little time and mental space left to innovate. i.e., the they lack capacity to test new products or services, which could be more profitable than existing ones. Therefore, a solid product portfolio analysis may lead to making a strategic decision to discontinue some products, freeing up some production capacity and allowing room to experiment with other, possibly more profitable product ideas.

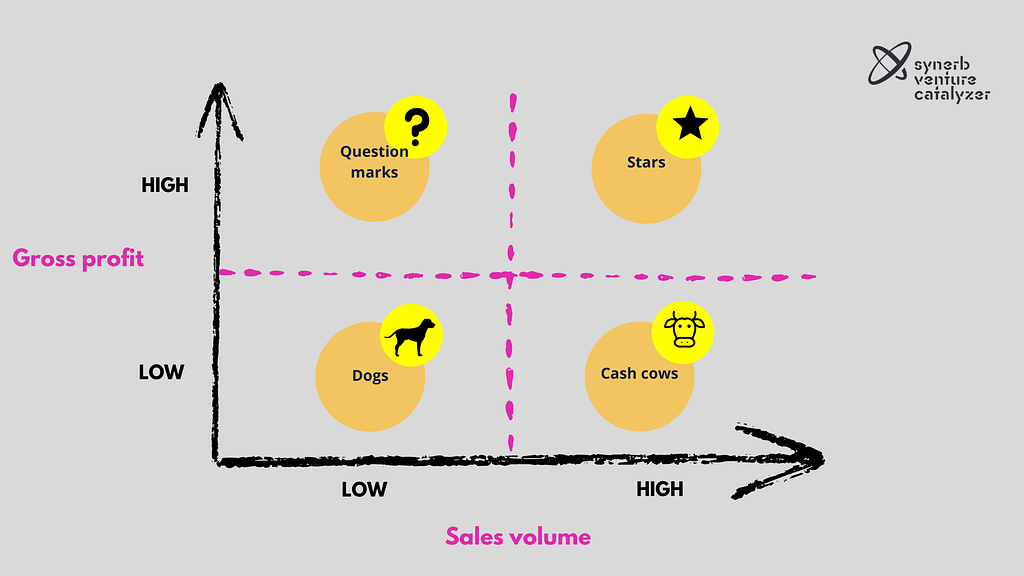

Let’s use the BCG matrix wisely!

An easy-to-use tool for doing a product portfolio analysis is the adapted version of the BCG matrix in the figure below.

Fig.1 – Adapted version of the BCG matrix

In the figure above, the two criteria for the portfolio analysis are shown on the X and Y axis.

The Gross Profit, calculated for each product, is the difference between the sales revenue and the costs directly attributed to that specific product. The gross profit shows us how much each product contributes to the overall financial sustainability of the company.

The Sales Volume is the total units sold of a product in a given period, usually in one year.

The BCG matrix thus helps us to divide our product portfolio into 4 major categories:

Flagship products or portfolio stars. These are those products from the portfolio mix that significantly contribute to the financial sustainability of the company, because their gross profit per unit is substantial. These products also rank high on the customer preference scale and are sold in large volumes. The dream of any social business is to have as many such products as possible in its portfolio, but it should be noted that to preserve the ‘star’ positioning of these products, the enterprise needs to invest resources into a significant and sustained promotion strategy.

Cash cows. These are products that have a low gross profit per unit. Because they are sold in large volumes, they contribute to the financial stability – positive cash-flow – of the business through the significant cash volume they generate.

Question marks. Products with a high gross profit per unit but with little interest from consumers and poor sales history. This may be the case for newly launched products that have not yet proven their value to the consumer, or it may be a star product that had lost its appeal to customers. The future of these products in the portfolio is uncertain, just as the category name indicates.

The “dogs’’ have a low gross profit and low sales levels. These products most often consume the resources of an organization and produce little value, and should be discontinued.

The BCG matrix is a dynamic tool. Assigning the portfolio products into these four categories is a flexible process. Product migration from one square to another is often inevitable, as we reclassify some. Perhaps, the most important feature of this tool is that it provides valuable input for strategic decisions made at the portfolio level. For example, we may decide not to invest resources in promoting our ‘cash cow’ type of products because they are in a solid position in the market. Instead, we decide to focus our efforts on keeping the ‘star’ products high in customers’ preferences for as long as possible, or we focus on converting ‘question marks’ into ‘stars’.

In the local Romanian market, a social enterprise usually operates with limited resources and high social costs. Therefore, it is important for these organizations to focus on selling “star” products or services that contribute to a large extent to the organization’s financial sustainability. The product portfolio analysis, used as a tool for strategic decision making, can many times make the difference between being profitable or operating at a loss, especially when the difference is only a few percent between the two indicators.

Conclusions

Today, more than ever, the social entrepreneurship sector is in the spotlight. The field attracts not only aspiring entrepreneurs with innovative ideas, but also a number of diverse stakeholders from the ecosystem: loyal customers of social businesses, sceptical consumers, intermediary organizations, impact funders or think-thanks studying the field. Their interest for the field manifests as a genuine desire to understand the successful social enterprise models and to decipher how success is achieved.

The most successful, financially sustainable social ventures in the world, which on the long run are able to fulfil their social missions, understood that in order to cope with the pressure of the social costs, they need to regularly use complex financial analysis when making strategic, sustainability-related or operational decisions.

These sound financial practices often depend on the social entrepreneur’s willingness and discipline to practice a knowledge-based management and make evidence-based decisions.

Through our work at Synerb, we constantly encourage leaders and managers to seek to understand the meaning of complex business data, from the community and customer feedbacks, to variations of the financial and social impact indicators.

To stand the test of time and achieve a substantial social impact, we believe organizations must – first and foremost- improve their financial and operational performance. There is no better way to promote the principles and values of social economy than achieving a solid social impact, backed by solid operational and financial metrics.

Finally, the success of a social enterprise can also be measured by its longevity and the social and financial impact it has on several generations of employees, beneficiaries or on the people whose lives have been greatly improved by the organisation.

*

[1] You can read more about the blue ocean concept here: https://www.blueoceanstrategy.com/what-is-blue-ocean-strategy

*

Related articles on the financial management of social enterprises:

![]() A brief financial guide for social enterprises seeking an investment

A brief financial guide for social enterprises seeking an investment

![]() An introduction to the cost of social mission

An introduction to the cost of social mission